Who won what? An analysis of the EU electricity market reform

Who won what? An analysis of the EU electricity market reform

How CfDs could cement France status as Europe’s low energy cost manufacturing center

Key Points:

France and Germany resolved a dispute over applying CfD to the nuclear fleet in the EU electricity market reform.

CfD guarantees electricity prices, with low strike prices for existing French nuclear units, potentially boosting French government revenues.

The challenge lies in designing a scheme to distribute CfD revenues that avoid EU competition distortions.

Combining with France's transmission cost advantage, the CfD further enhances France’s status as Europe's low-cost energy hub for manufacturing.

For months, France and Germany were locked in a standoff over a reform affecting the European Union's electricity market. France sought to implement a state-backed electricity price guarantee mechanism known as Contract-for-Difference (CfDs) to fund the life extension of its existing nuclear fleet. Germany opposed this move, concerned that it would enable France to subsidize its industry using the revenues generated.

A compromise was finally struck this week. The agreed text permits France to apply CfDs to its existing nuclear fleet, while also giving the European Commission the authority to ensure that CfD's application doesn't create "distortions to competition and trade in the internal market" arising from revenue distribution.

Why is the application of CfD to the existing nuclear fleet so significant? To understand this, we need to delve into the CfD mechanism, the role of existing nuclear power in lowering electricity costs, and how this provides France with a growing economic advantage over its neighbor.

CfD as a State-Backed PPA

CfD offers a price guarantee for each MWh generated by a power plant. The guaranteed price, also known as the strike price, is determined through periodic auctions, or occasionally through direct bilateral negotiations between the government and the generator. Taxpayers compensate the generator for the gap between the strike price and the wholesale market price when the market price falls below the strike price. When the market price exceeds the strike price, the generator refunds the excess to electricity customers. Essentially, CfD functions as a state-backed power purchase agreement (PPA).

CfDs aren't a novel concept; they are already utilized by numerous European countries, with the United Kingdom being a prominent example. It serves as a means to support the growth of renewable energy generation by providing wholesale price certainty and establishing the government as the counterparty to the agreement. During periods of high electricity prices, electricity consumers can also benefit if surplus funds collected from generators are distributed back to them. The EU's electricity market reform mandates the use of CfD as the sole state-backed price support mechanism moving forward.

Applying CfD to the Existing French Nuclear Fleet

Until now, CfDs in Europe have primarily been applied to new generation projects, constituting only a small fraction of national generation. Historically, the strike prices for these CfDs have often exceeded wholesale power prices, which, apart from a temporary shift due to the war in Ukraine last year, contributed to increased government expenditures or, in the case of the UK, electricity bills.

Applying CfDs to the existing French nuclear fleet represents a substantial departure from the norm for two critical reasons. Firstly, the sheer scale of French generation covered by the CfD scheme would be extensive. Figure 1 illustrates that the volume of electricity under CfD is projected to increase from 12% in 2026 to over half of the total projected demand by 2033. This assumes that CfD applies solely to existing nuclear units due for maintenance for a 10-year life extension starting next year, with no retroactive application to refurbished units and no additional CfD for further 10-year extensions.

Source: 8760 analysis based on EDF’s nuclear maintenance schedule and RTE (France’s Electricity Transmission System Operator) electricity demand projection in Reference scenario. The percentage figure represents nuclear CfD generation as a percentage share of national demand.

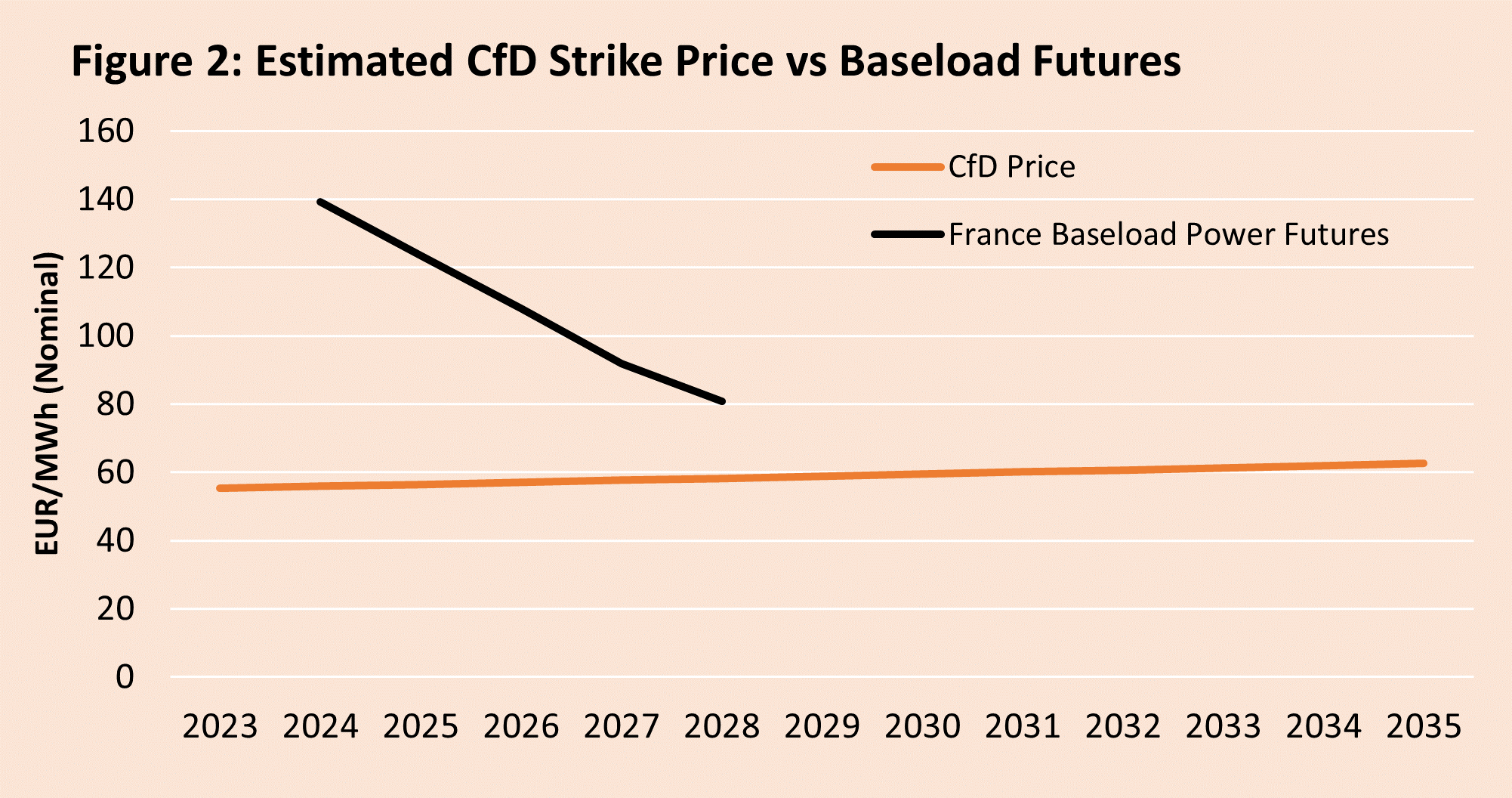

Secondly, the negotiated strike price for CfDs on the existing nuclear fleet is anticipated to be low. My estimate places the likely CfD price at around €56/MWh in 2025, which is less than half of the current traded price for French electricity delivery in 2025 (€123/MWh). Consequently, unlike other CfD schemes, the French scheme for existing nuclear power would generate substantial revenues for the government. This is a concern for Germany.

Source: 8760 analysis based on EDF’s estimate of capital costs for Grand Carénage Phase II program, OPEX from EDF’s segmental reporting for UK nuclear adjusted for lower transmission charges in France, EDF’s cost of capital from EDF consolidated financial statements 2022, France Baseload Power Futures from EEX as of 17 October 2023. CfD CAPEX calculation assumes 10-year cost recovery and 75% capacity (load) factor. OPEX except fuel escalates by 2.25% a year.

State-Aid Rules Constrain France’s Use of CfD Proceeds

Revenues generated by the French nuclear CfD scheme must be distributed to final electricity customers, as stipulated in article 19(b) of the agreed reform. To address Germany's concerns, the reform includes a restriction in paragraph 1a of article 19(b) that emphasizes the need to avoid competition distortions and trade disruptions in the internal market due to the distribution of revenues from CfDs.

Articles 107 and 108 of the Treaty on the Functioning of the European Union (TFEU) pertain to regulations governing state resources (state-aid) favoring domestic firms, with the aim of preventing competition distortions across the European Union. Enforcement of these state-aid regulations ensures a level playing field for businesses within the EU.

The central issue is whether the distribution of revenues from the CfD scheme would indeed distort competition within the EU. It remains uncertain how France will design its scheme, and any design would necessitate negotiations with the European Commission for state-aid clearance.

For this analysis, I assume that the French government will return CfD revenues to customers in the form of a price credit. The price credit would be uniform for each unit of consumption, based on the total CfD revenues divided by total French electricity consumption. Furthermore, I assume that CfD will only apply to a nuclear unit once it has completed the life-extension maintenance.

Source: 8760 analysis based on France and Germany baseload power futures prices from EEX as of 17 October 2023. Projected annual CfD revenues are divided by projected French power demand to derive CfD price offset on France baseload power prices.

Based on this analysis, the price differential between electricity users in France and Germany is marginal at the program's onset, growing to €8/MWh by 2028 and €10/MWh as more units are retrofitted and included in the CfD scheme (see Figure 3). As an example, a €10/MWh reduction in electricity prices reduces the cost of producing electric arc furnace steel by €4.3/tonne or approximately 0.7% of the final price. Given the current steel pre-tax profit margin of 2.8%, the €10/MWh reduction would boost profits by 25% (0.7% / 2.8%).

This appears to introduce a distortion in EU-wide competition, especially considering that the benefits ripple through the supply chain, from steel manufacturing to final car assembly. This is why the additional text in article 19(b) has more significant implications than it may initially seem. Designing a CfD revenue distribution scheme that avoids competition distortions within the EU is expected to be challenging for France.

Don’t Overlook Transmission

CfD's impact is limited to the prices paid by customers for electricity, representing just one component of electricity bills. Other factors include charges covering the costs of electricity networks and various policy fees.

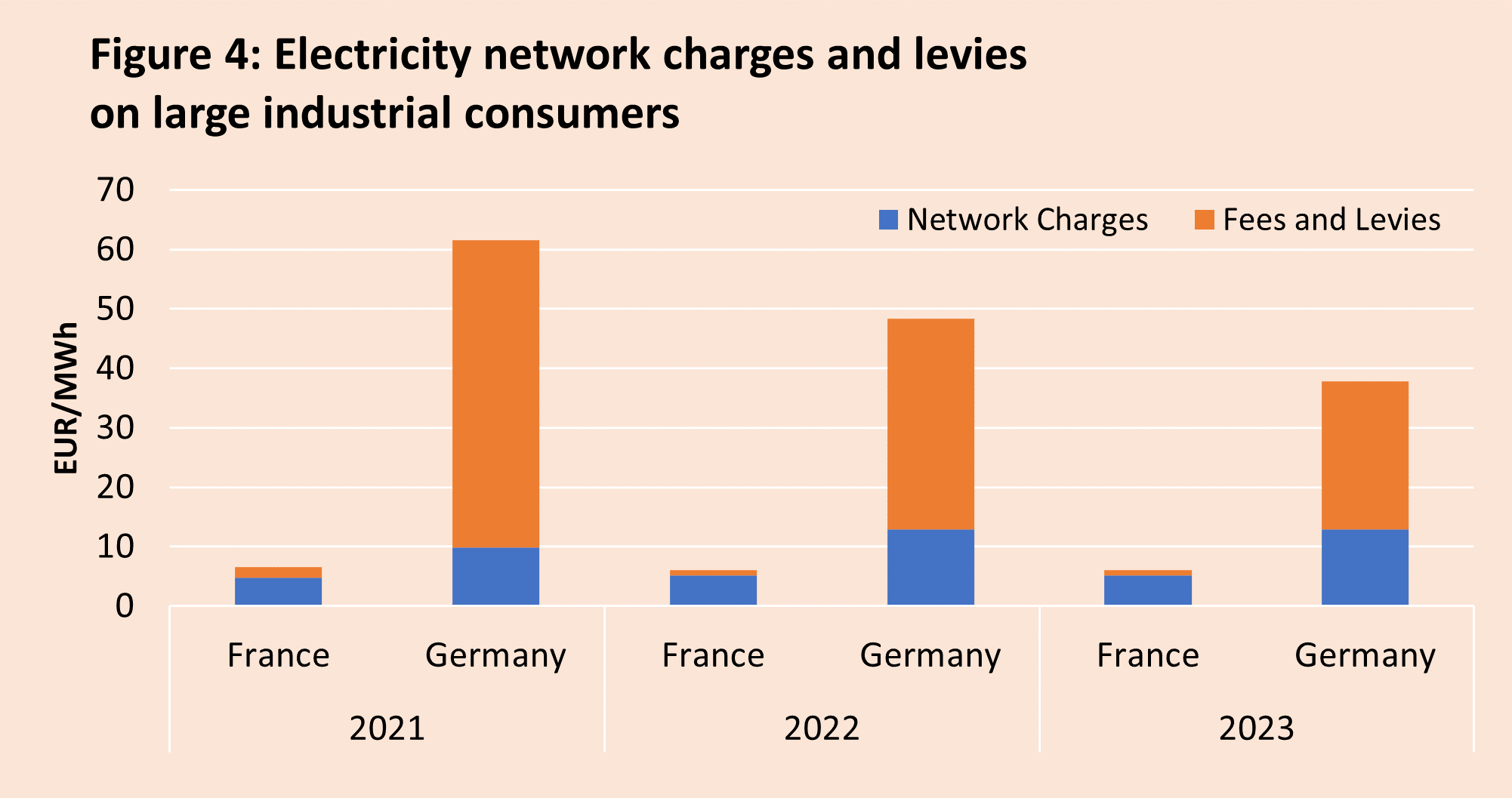

Figure 4 underscores that France maintains a clear advantage with significantly lower network charges, fees, and levies for large industrial consumers. Germany, on the other hand, has been implementing measures to reduce policy fees imposed on electricity consumers, the most recent being the elimination of the levy to fund renewable energy support costs (the EEG levy) from 2023.

Source: Eurostat table nrg_pc_205_c for consumption of 150GWh/year and above

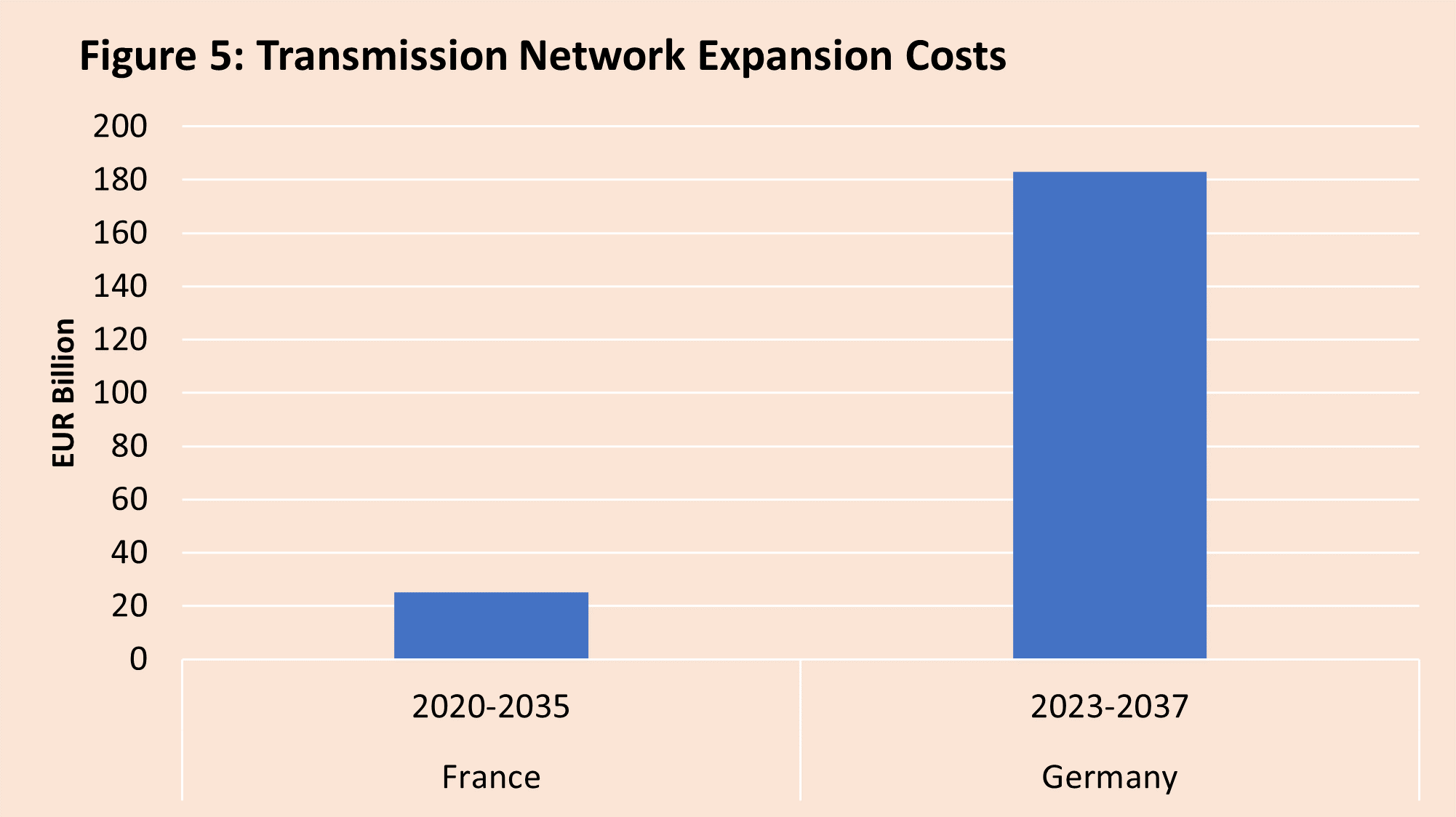

However, network charges in Germany are poised to rise significantly faster than in France. France anticipates around €25 billion in transmission investment costs by 2035, compared to Germany's planned expenditure of €183 billion by 2037. The lower cost in France is attributed to slower load growth, with most residential and commercial heating already powered by electricity. In contrast, 80% of heating in Germany relies on fossil fuels, and the shift to electricity drives increased electricity demand, necessitating the construction of more transmission lines.

Source: French transmission network development plan 2019 edition and Germany grid development plan electricity 2037 with outlook 2034, second draft

The expenses associated with these transmission investments will be borne by electricity consumers. Germany's power demand is expected to be roughly 50% higher than France's in the mid-2030s, according to transmission network development plans. However, transmission expansion costs will be approximately nine times higher per Figure 5. Consequently, we can expect transmission charges in Germany to grow around six times faster than in France (9/1.5). This provides French manufacturers with a substantial energy cost advantage.

This would also bode well for micro-grid developers in Germany, as avoiding grid charges could offer substantial savings to German manufacturers. Although any transmission costs avoided by manufacturers would ultimately be borne by residential and commercial customers, further raising their bills.

The CfD enhances France’s electricity cost advantage

In summary, the implementation of CfD reinforces France's electricity cost advantage, solidifying its position as Europe's low-cost manufacturing center for energy-intensive industries. The additional state aid provision concerning CfD revenue distribution however is likely to complicate approval.

I would be interested to see how this scheme compares to say Ontario's state backed PPA system for existing nuclear.

https://www.brucepower.com/who-we-are/delivering-transparency-and-trust/

Something that is notable in Ontario that may or may not occur in France is that the "market" price for electricity is in fact quite low due to the various transmission constraints that limit wheeling power to neighboring jurisdictions.