Renewable Energy Stocks Tumble: Is It Game Over?

Renewable Energy Stocks Tumble: Is It Game Over?

Sector now re-priced for the new environment. Bad for existing shareholders, but opportunities for new buyers.

Key Points:

Renewable share prices declined significantly in recent weeks.

The value of PPAs held by renewables companies are sensitive to rising interest rates.

Higher interest rates reduce debt-financing options, pressuring growth prospect for incumbents.

Legacy PPAs are now re-priced.

It is hard to miss the drop in renewable share prices over the past few weeks. Shares of NextERA Energy Partners (NEP) led the pack, sinking by 54% over the past two weeks, while Brookfield Renewable Partners (BRP) declined by 17% over the same period. In fact, the entire renewable power generation sector has declined by more than 40% since the beginning of this year (see Figure 1). To understand this, let’s examine the business model of renewable generation companies and how it is influenced by interest rates.

Source: 8760 analysis

Note: The price index is based on taking an equal-weighted average of daily returns across renewable generation companies with shares listed in the United States.

Renewable Generation Companies as Car Leasing Companies

In many ways, renewable generation companies operate much like a car leasing company. They buy solar panels upfront and then enter into an agreement (power purchase agreement, PPA) to charge their customers an ongoing fixed fee ($/MWh) for using the electricity generated from the solar farm over a fixed period. The fixed fee is designed to cover the costs of developing and building the solar farm, interest on the debt taken to pay the upfront cost, and, of course, profits. Since the fixed fee is agreed upon upfront, the profit rate is also locked in at the beginning for the duration of the PPA.

These PPAs can last a long time; the average term of the PPAs in BRP's portfolio is 14 years.[1] Figure 2 shows rapid growth in annual renewable capacity additions in the US during the low-interest-rate era between 2020 and 2022, suggesting that a significant portion of the outstanding PPAs would have been executed during this period of low interest rates. This means that the profit rate locked into those contracts would also be relatively low.

Source: Berkeley Lab, Utility-Scale Solar 2023

PPAs in High Interest Rates Environment

These PPAs behave like bonds in the sense that their holders receive a relatively fixed stream of income[2] over the contract's duration. The income streams in later years are worth less today as interest rates increase. Therefore, like bonds, the current market value of a fixed-price PPA from the PPA seller's perspective also varies with interest rates. The higher the interest rates, the lower the market value of those PPAs from the PPA seller's perspective. It's more complicated from the buyer’s point of view, but I am not covering that here; ask your local energy market consultants.

How sensitive is the value of PPAs to rising interest rates? Figure 3 shows the market value (net present value) of a stylized 15-year PPA that was executed at a 5% nominal interest rate. A 200 basis points increase in the interest rate reduces the market value of the PPA by about 17%. So the short answer is: a lot.

Source: 8760’s proprietary “A Man with Excel Spreadsheet” model (AMWES)

Note: Assuming fixed 12% equity IRR, 80% leverage, and 2-year tail.

Real interest rates for longer-duration bonds were largely range-bound for the first half of the year, reflecting the market's belief in an impending monetary policy pivot that never materialized. Real interest rates on longer-duration bonds rose significantly after August as the "higher for longer" narrative took hold. As of last week, the real interest rate on the US 10-year government bond is trading near 2.5%, a nearly 150 basis points move since April (see Figure 3). Interest rates are staying high for longer due to the unprecedented level of capital expenditures, requiring more capital. For a more detailed exploration of this issue, see our previous article, "Who’s Gonna Build It?"

Source: Federal Reserve Bank of St. Louis

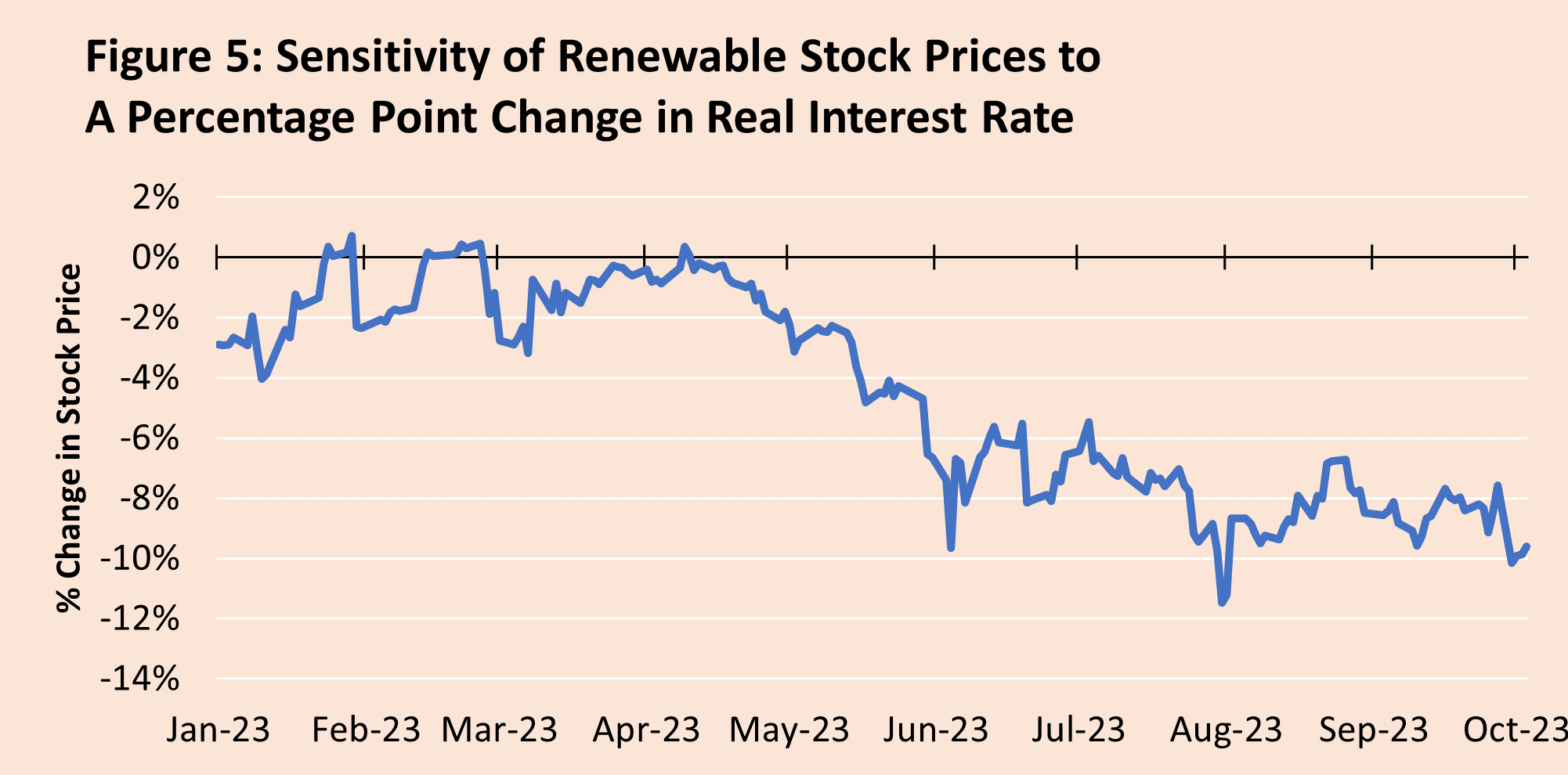

The market largely ignored the impact of real interest rates for most of the first quarter. This changed dramatically after April when renewable stocks became increasingly sensitive to changes in the real interest rate (see Figure 5). Now, a 1 percentage point change in the real interest rate translates to around a 10% decline in renewable shares on average. Gradually, then suddenly, I guess.

Source: 8760’s proprietary “A Man with R Studio” model (AMR)

Note: 60-day rolling regression of daily renewable stock composite returns (see Figure 1) against daily S&P500 returns and daily changes in the US 10-year real interest rate.

High Interest Rates Dent Growth

So far, this has been a long-winded way of saying renewable stock prices tanked because of higher real interest rates, but that is not the only factor. High interest rates also reduce the amount of debt renewable generation companies can use to finance new projects. This is because lenders typically require a buffer between the cash generated by the project and the cash required for annual interest payments and principal paydowns (debt-service coverage ratio, DSCR).[3]

Higher interest rates increase annual interest payments, necessitating a larger buffer. Figure 6 shows the stylized impact on the maximum level of leverage a project can assume at a given interest rate. The impact is most pronounced on projects where the increased financing costs cannot be passed on to customers. Lower leverage means a higher equity investment in a project (see a slide from Sunrun Q2 financial results presentation for a real-life example). However, with plummeting stock prices, issuing new equity to fund growth would be highly dilutive to existing shareholders, and so it is unlikely to happen. As a result, the market revises its expectations for future growth downward. The prospect of lower growth further pressures share prices, creating a bit of a catch-22.

Source: 8760 AMWES

Note: Based on 18 years amortized debt, 80% leverage, 1.3 DSCR

Source: Sunrun Q2 2023 Financial Results Presentation

But the Game is Not Over

Does this mean that the game is over for renewable generation? The answer is no. The issues discussed here primarily affect existing operators who are now saddled with legacy PPAs. These legacy PPAs have been repriced to reflect the current cost of capital. New PPAs being negotiated today will embed today’s cost of capital and could prove to be a good investment for long-term income. 8760 will look at why this environment makes solar sexy again in a forthcoming article later this month.

[1] Brookfield (June 2023), “Corporate profile”, available at https://bep.brookfield.com/sites/bep-brookfield-ir/files/brookfield/bep/presentation/brookfield-renewable-corpprofile-june-2023-vf2.pdf

[2] There will be variations due to production volumes affected by the sun, the wind, and recently quality issues associated with wind blades.

[3] I am not delving into the technicalities of project finance in this article; please consult your local corporate finance advisory firms.

Great Article.